The basics of long-term disability insurance

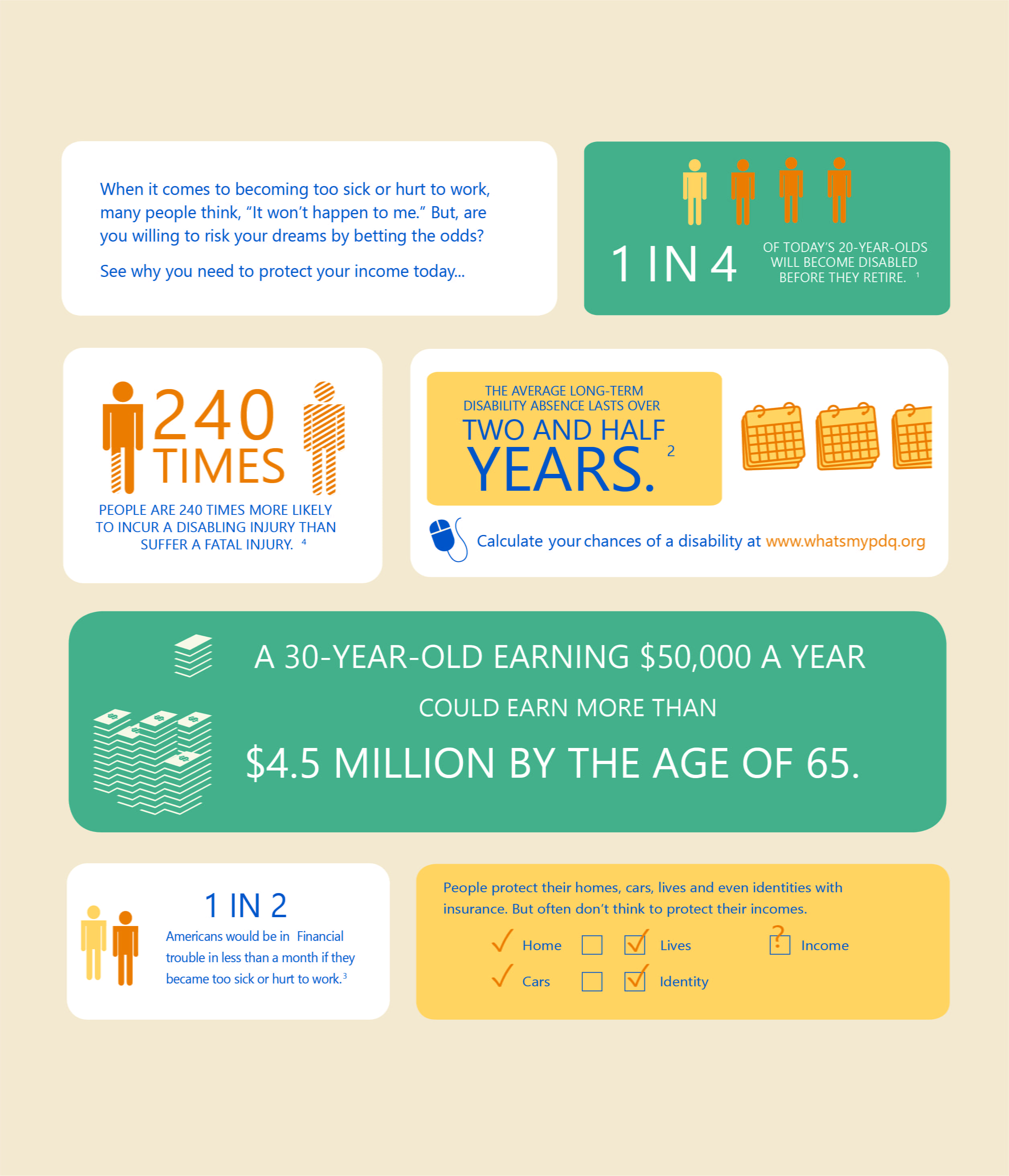

You may not realize the potential danger of becoming disabled. The U.S. Census Bureau estimates that you have a one in five chance of becoming disabled. Also, the average long-term disability (LTD) absence from work lasts 2.5 years, according to the Council for Disability Awareness (CDA). That’s a long time to survive without a steady income.

Buying individual disability insurance

If your employer does not offer group disability insurance, or if you feel your existing group policy does not provide adequate coverage, you may want to consider buying an individual long-term disability policy.

Most policies are sold on a “non-cancellable” or a “guaranteed renewable” basis, according to the Insurance Information Institute (III). With a non-cancellable policy (which requires an initial medical exam), the insurer cannot cancel the coverage or raise your premiums. If you buy a policy on a guaranteed renewable basis, the insurer cannot cancel the coverage as long as you pay premiums. Most individual policies also have features that allow benefits to keep pace with inflation or gradual salary increases, such as a cost of living adjustment (COLA), which adds a percentage to your benefit each year.

Is your paycheck Protected ?